Boat financing works similarly to auto loans, with lenders offering terms typically ranging from 10 to 20 years, depending on the loan amount and your credit score. Most dealers in our Blazer Boats network can help you navigate financing options, making it easier than ever to get behind the wheel of your dream boat.

You’ve found the perfect bass boat or bay boat. Maybe it’s a 650 Pro Tour that’ll give you the tournament edge you’ve been chasing, or a versatile PureBay 2400 that handles everything from shallow flats to nearshore runs. Now comes the question every serious angler faces: how do you turn that dream boat into a reality?

Understanding boat financing doesn’t have to be complicated. Like buying a car or recreational vehicle, purchasing a new boat involves working with lenders to spread the purchase price across manageable monthly payments. This guide breaks down what you need to know before walking into your local dealer, so you can spend less time worrying about paperwork and more time planning your next trip to that secret fishing spot.

Understanding Boat Loans

A boat loan functions much like an auto loan or personal loan. A financial institution provides the funds to cover your boat purchase, and you repay that loan amount plus interest over an agreed period. The boat itself typically serves as collateral, meaning the lender can reclaim it if you default on payments.

Unlike buying a car, boat loans often come with longer terms because of the higher purchase price involved. While a typical car loan might run 5 to 7 years, boat financing can extend from 10 to 20 years, depending on the total cost and your financial situation. This longer term helps keep your monthly payment within reach, though it’s worth noting you’ll pay more in total interest over the life of the loan.

Where to Get Boat Financing

Several types of lenders offer boat loans:

- Marine lenders: Specialize in boat and personal watercraft financing, often offering competitive rates and flexible terms tailored to recreational vehicles

- Banks and credit unions: Your existing financial institution may offer boat loans, and credit union members often find lower APRs through their member services

- Dealer financing: Many boat dealers work with multiple lenders to help customers secure financing right at the point of sale

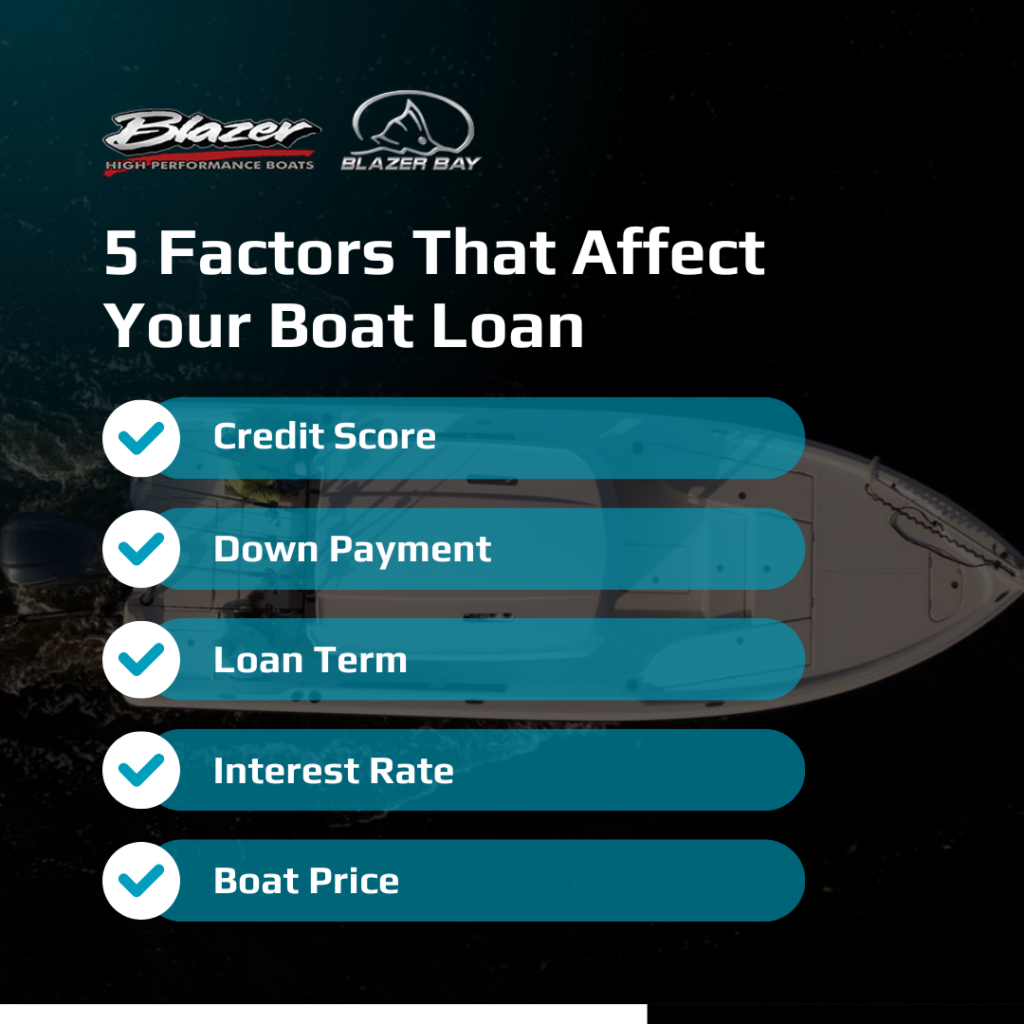

Key Factors That Affect Your Loan

Credit Score and History

Your credit score plays a significant role in determining both credit approval and the interest rate you’ll receive. Borrowers with excellent credit typically qualify for the lowest rates and best terms, while those with lower scores may face higher annual percentage rates or need a larger down payment.

Before starting the loan application process, consider pulling your credit report to understand where you stand. Addressing any errors or paying down existing debt can improve your score and help you secure better rates when it’s time to apply.

Down Payment

Most lenders require a down payment of 10% to 20% of the purchase price. A larger down payment reduces your total loan amount, which means lower monthly payments and less interest paid over time. It also demonstrates financial stability to lenders, potentially helping you secure loan approval with more favorable terms.

Loan Term

The loan term directly impacts your monthly payment. A longer term spreads payments across more months, making each one smaller. However, extending the term means paying more total interest. For boats priced under $50,000, terms typically range from 10 to 15 years. Larger vessels may qualify for terms up to 20 years.

When comparing options, use a loan calculator to see how different terms affect both your monthly payment and total cost. Finding the right balance between affordable payments and reasonable total interest is key to smart financing.

Interest Rate

Interest rates will depend on factors such as your credit score, debt-to-income, and money being put down on the loan. Rates can vary significantly between lenders, so shopping around is worth your time. Even a small difference in annual percentage rate adds up over a 15 or 20 year loan.

Be aware that boat loan rates are generally higher than mortgage rates but often comparable to RV loan rates. The boat being used as collateral helps keep rates lower than unsecured personal loans.

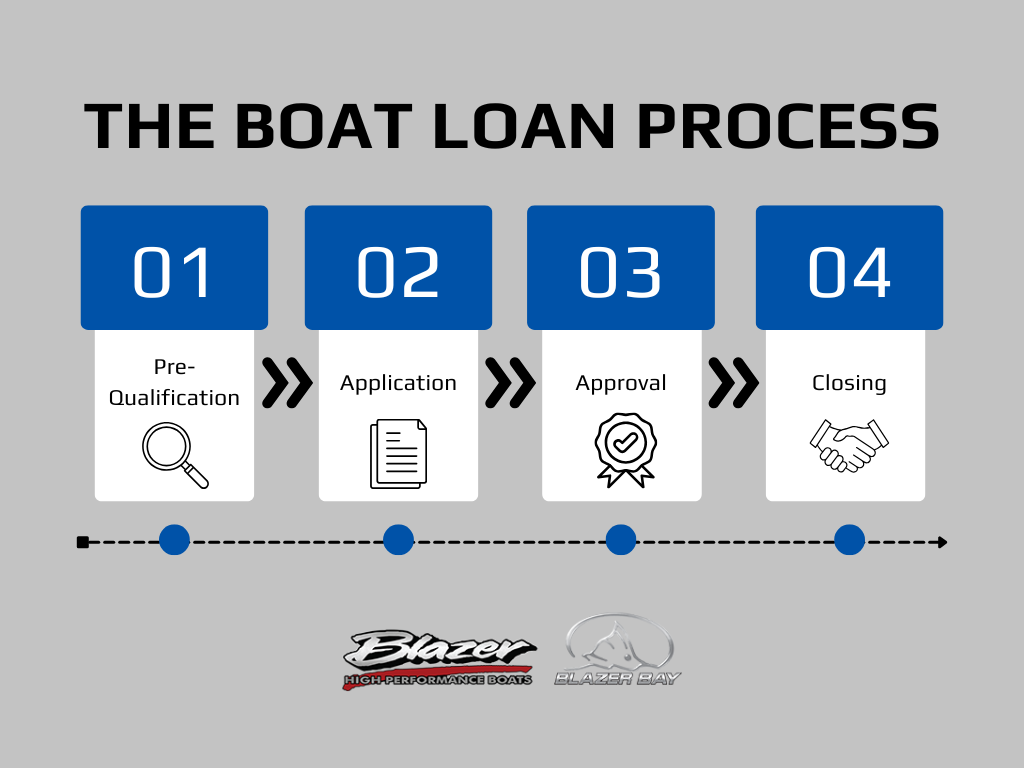

The Loan Application Process

The loan process for a boat purchase follows a familiar path if you’ve ever financed a motor vehicle. Here’s what to expect:

- Pre-qualification: Many lenders offer pre-qualification, giving you an idea of rates and terms before you commit. This step often involves a soft credit check that won’t affect your score.

- Formal application: You’ll provide detailed financial information including income verification, employment history, and existing debts.

- Credit approval: The lender reviews your application and credit history. Some lenders offer same-day approval for qualified buyers.

Closing: Once approved, you’ll sign final documents. The lender disburses loan proceeds to the dealer, and you take ownership of your new boat.

What to Watch For

Before signing any financing agreement, pay attention to these details:

- Prepayment penalties: Some lenders charge fees if you pay off your loan early. Look for loans without prepayment penalties if you might refinance or pay ahead

- Origination fees: These upfront charges can add to your total cost. Ask lenders to explain all fees included in your loan

- Insurance requirements: Lenders typically require comprehensive boat insurance for the life of the loan

- Total cost: Compare the total amount you’ll pay over the life of the loan, not just the monthly payment

Tips for Getting the Best Rates

Securing competitive rates on your boat loan takes some preparation:

- Check your credit report and address any issues before applying

- Get quotes from multiple lenders including banks, credit unions, and marine specialists

- Consider making a larger down payment to reduce your loan amount

- Choose the shortest loan term you can comfortably afford

- Ask about any special programs or seasonal financing promotions

- Work with finance experts who understand the marine industry

Get Started with Blazer Boats

At Blazer Boats, we’ve been building high-performance bass boats and bay boats by hand since 1978. While Blazer Boats doesn’t offer financing directly to consumers, most dealers in our Blazer Boats Dealer network offer financing options for boat purchases. Your local dealer can help you navigate the entire process, from reviewing financing options to finalizing your boat registration and paper title.Ready to find your dream boat? Explore our lineup of bass boats and bay boats, then contact your local Blazer dealer to discuss financing solutions that fit your budget. Our dealers work with you to make owning a hand-crafted, American-made Blazer boat a reality. The open waters are waiting.